Even if you exclude the double-digit contraction in revenues in 2009, the market has still been averaging only around half the annual growth that it achieved before the recession. The market analyst IHS does not expect growth to recover to the rates experienced before the downturn, adding that the low growth rates of recent years are the “new normal” for a maturing product market, which has also been affected by regional economic weaknesses.

IHS suggests that this market maturity is “long overdue” for a product that was introduced at about the same time the first Apple Macintosh computer. Improvements to VSD components and designs over the past 30 years are now becoming standardised in an increasingly competitive landscape, creating a commoditised product and driving down prices.

According to IHS, “inorganic” factors prolonged momentum in expanding drive markets, increasing the numbers of drives being attached to motors, by overcoming two significant barriers to adoption: awareness/understanding and upfront cost. While there has not been an abrupt decline in either of these factors, their waning influence in a maturing market has diminished the prospects for long-term growth.

“As the attachment rate of drives to motors moves closer to its apex, the growth in demand will understandably decelerate,” says IHS analyst, Kevin Schiller. “In addition, the higher drive attachment rate will also reduce future retrofit opportunities, which have recently provided lucrative demand in sizeable drive markets – such as the HVAC, food, beverage, and tobacco sectors.”

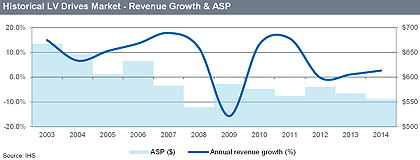

Although growth in the LV drives market has recovered since 2009, it is still lower than it was before 2009, while drives prices are lower than they were previouslySource: IHS

The deceleration in the demand for drives is more significant in markets with high drive-motor attachment rates, such as Japan, Western Europe and North America. IHS forecasts that these markets will increase revenues with a CAGR of only about 4% between 2014 and 2019.

iIn the short-term, incentives for retrofits will continue to lift growth rates for LV drives above other industrial automation equipment, but a trend towards evaluating energy efficiency at a system level is expected to commoditise the drives markets further in these developed regions. Because they also have sizeable discrete markets, machine-building sectors that export to other regions are forecast to provide the biggest opportunities for growth.

Markets with lower drive-motor attachment rates – such as the Asia-Pacific region (outside of China) and Latin America – are forecast to have the best opportunity for long-term growth, in domestic process sectors and as a destination for discrete machinery exports. Revenues for LV drives in these markets are expected to grow with a CAGR of at least 7% between 2014 and 2019.